October was a quiet month for composites. Demand from most customers markets was below the seasonal average. Automotive could scarcely make any ground good, though the utility vehicle segment continued to order well.

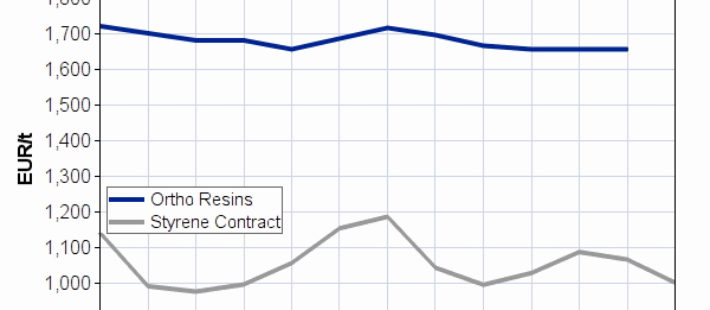

With demand expected to remain soft and styrene pointing more sharply downward, resins prices will surely slip back in November, potentially by about half of the feedstock downswing – this especially as the slight decline in the October SM contract did not make much of an impact initially. Also, worth noting is that phthalic anhydride just barely remained stable. The Q4 contract for maleic anhydride had not yet been fixed at press time.

Glass fibre products likewise showed little momentum last month and look likely to move sideways up to the end of 2019. The markets are well supplied, and demand from the automotive industry undoubtedly will not budge before the Christmas and New Year holidays.

Source: EuCIA, Plastic Information Europe